This summer’s wildfires, covering over 300,000 hectares, catalysed a sweeping 10-point climate emergency plan from Prime Minister Pedro Sánchez on 1 September 2025. At its core is mandatory carbon reporting – a major shift from previous voluntary measures and part of Spain’s broader effort to align with European sustainability reporting standards.

The legal framework explained

Spain’s new carbon reporting rules are primarily established by Royal Decree 214/2025, which transforms the carbon footprint registry into a binding requirement. This national legislation builds on the foundations of:

- Law 7/2021 on Climate Change and Energy Transition, which sets Spain’s broader climate targets and authorises mandatory disclosure of carbon data.

- The Non-Financial Reporting Directive (NFRD), which originally required large companies to disclose certain ESG information.

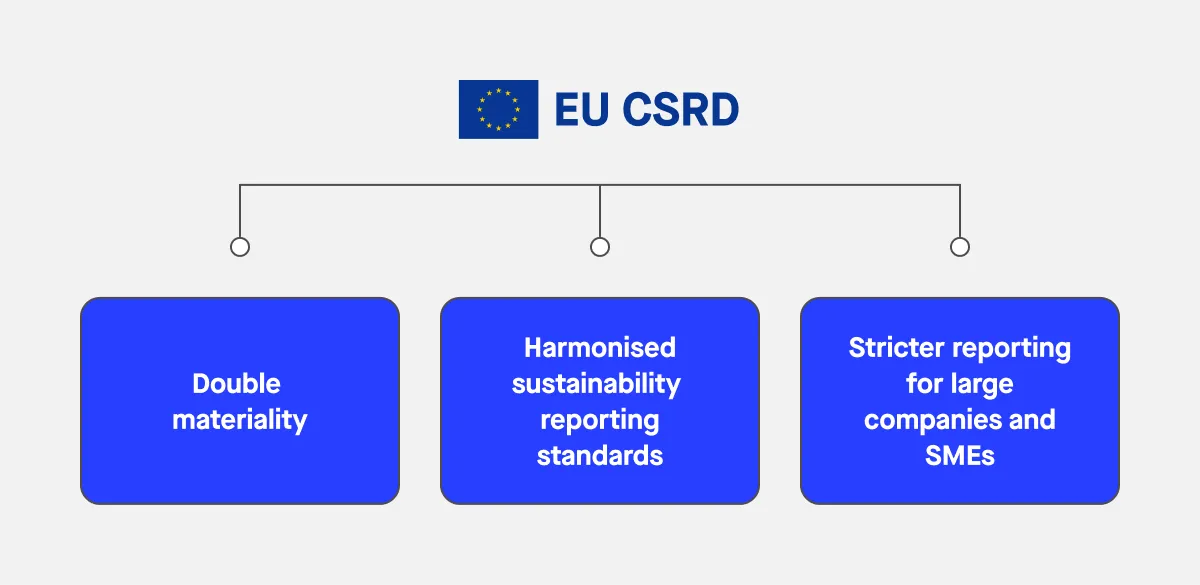

- The Corporate Sustainability Reporting Directive (CSRD), which strengthens the scope of sustainability reporting requirements across the European Union and introduces detailed sustainability reporting standards under the ESRS (European Sustainability Reporting Standards).

Who’s covered by the new rules

Royal Decree 214/2025 applies to:

- Private companies that fall under Law 11/2018 (Spain’s transposition of the NFRD). This means companies with over 250 employees and either assets > €20 million or turnover > €40 million for two consecutive years. These are considered public interest entities because of their size and impact.

- Public entities, including ministerial departments, autonomous bodies, Social Security agencies, and other government institutions.

In total, around 4,000 public and private entities will be required to comply. SMEs are not automatically included, though they may be indirectly affected through supply chain demands or access to finance.

Sustainability reporting requirements: What businesses need to report and when

- Reporting begins in 2026, using 2025 data, and covers:

- Scope 1 (direct emissions)

- Scope 2 (indirect emissions from energy)

- Scope 3 (value-chain emissions) becomes mandatory from 2028 for large entities.

- Reduction plans: From 2026, companies must publish five-year greenhouse gas reduction plans with measurable sustainability targets, hosted on their website or in their sustainability reporting documents.

- External assurance is required in certain cases: for large companies, when applying for subsidies, or if Scope 3 makes up a significant share of emissions.