CSRD compliance timeline: what you need to know

Compliance is being phased in from 2024 through 2029:

| Company type |

First reporting year |

Publication date |

| Companies previously under NFRD |

2024 |

2025 |

| Large public interest entities (new to mandatory reporting) |

2025 |

2026 |

| Listed small and medium enterprises |

2026 |

2027 (opt-out until 2028) |

| Non-EU companies |

2028 |

2029 |

Why you can’t wait: The CSRD requires companies to report their sustainability impacts in a standardised digital format, which aims to enhance comparability and reliability of sustainability data across different organisations. Building that infrastructure takes time.

Six critical CSRD requirements

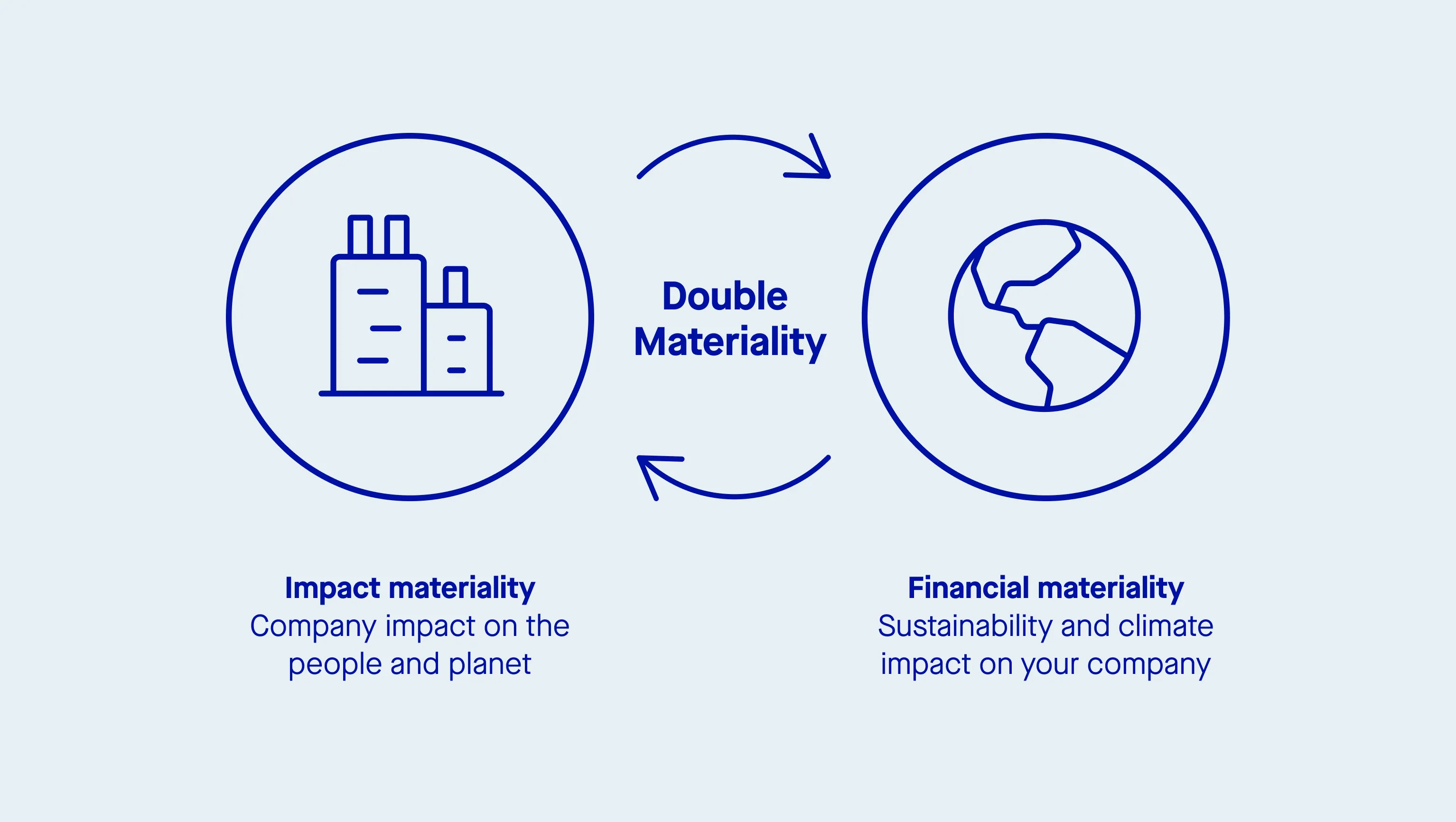

1. Double materiality assessment

What it means: Double materiality requires organisations to report on:

- The impact their businesses have on sustainability matters (impact materiality)

- The impact that sustainability matters have on their finances (financial materiality)

This is a fundamental departure from single materiality frameworks, which focus only on financial risks to the company.

What you need to do:

- Engage stakeholders across your entire value chain

- Identify material sustainability topics requiring disclosure under ESRS

- Document your assessment process for audit purposes

Most organizations conduct a double materiality assessment as a first step toward compliance with the CSRD, ensuring they understand both their sustainability impacts and financial risks associated with those impacts.

2. European Sustainability Reporting Standards (ESRS)

The framework you’ll report under:

The ESRS were officially adopted by the European Commission on 31 July 2023, and published in the Official Journal of the EU in December 2023, making them legally binding.

Structure:

- 12 standards covering sustainability matters

- Four categories: Cross-cutting, environmental, social, and governance

- Four pillars per topic: Governance, strategy, risk management, metrics and targets

Companies must disclose information following the same structure as financial reporting, embedding sustainability into core business processes and the management report.

3. Value chain reporting

The challenge: CSRD mandates that companies report sustainability information across their entire value chain, including:

- Upstream: Emissions from producing or transporting goods or materials you purchase

- Downstream: Emissions from customers using or disposing of your products

The data problem:

Research shows that 69% of businesses struggle with supplier data collection . This is the single most critical barrier for businesses worldwide, particularly for Scope 3 reporting under CSRD.

Why it’s difficult:

- No standardised data formats

- Variable supplier engagement across geographies

- Limited regulatory pressure on smaller suppliers

- Manual collection processes that don’t scale

For most businesses, Scope 3 emissions and social and environmental impacts in the value chain are the largest and most complex aspects of sustainability performance.

4. Climate transition plans and net zero alignment

What CSRD requires:

Companies must disclose their climate transition plans, aligning with the 2050 climate neutrality objective established under the European Green Deal.

Starting in 2025, the CSRD mandates that businesses have a Paris Agreement-aligned emissions reduction plan to reach net zero by 2050.

What your plan must include:

- Science-based targets for Scopes 1, 2, and 3

- Specific sustainability targets and timelines

- How you will limit global warming to 1.5°C

- Concrete actions and capital allocation

- Financial implications and business strategy alignment

- Governance structures and company board oversight

This goes beyond aspirational net emissions goals. You need to show how your business model and business strategy will deliver climate neutrality.

5. Mandatory assurance and audit requirements

A fundamental shift: For the first time, sustainability data must be independently audited to ensure its accuracy and reliability.

The standard:

- Initially: Limited assurance (similar to financial statement review)

- Over time: Reasonable assurance (same standard as financial reporting)

What this means for data quality:

According to global research, 41% of organisations report improved audit outcomes from better carbon data management . High-quality, auditable sustainability information is rapidly becoming a competitive necessity, not just a compliance requirement.

6. Penalties for non-compliance

Member states can impose penalties on companies that omit information or submit non-compliant reports.

Examples:

- Germany: Financial penalties up to €10 million or 5% of annual turnover

- France: Directors may face imprisonment for failing to provide essential data to auditors

The consequences of getting this wrong are significant.

The current state of readiness: three major challenges

Challenge 1: Spreadsheet dependency

59% of global businesses still rely on spreadsheets for carbon accounting .

The risks:

- Data accuracy issues

- Version control problems

- Not audit-ready

- Difficult to scale

As CSRD reporting requirements grow more granular, manual spreadsheet processes are increasingly difficult to maintain. A strong ESG data foundation can help ease reporting, make disclosures auditable, and prepare organizations for upcoming regulatory changes.

Challenge 2: Resource constraints

32% of businesses lack sufficient internal resources for sustainability reporting .

Why this is critical:

- Double materiality assessments require cross-functional expertise

- Value chain reporting demands supplier engagement capacity

- Mandatory assurance requires robust data governance

Automation and integrated platforms are essential to help teams accomplish more with existing resources.

Challenge 3: Time investment

65% of organisations complete annual reporting within three months , but more than one in four spend three months or longer on a single reporting cycle.

That burden will grow as:

- CSRD requirements expand

- Assurance standards tighten

- Multi-framework reporting becomes standard