You’ll learn:

-

Which companies are covered by CSRD Wave 2

-

Key changes from the Omnibus proposals

-

How double materiality works in practice

-

Steps to get ready for reporting

-

How to turn compliance into business value

Which companies are covered by CSRD Wave 2

Key changes from the Omnibus proposals

How double materiality works in practice

Steps to get ready for reporting

How to turn compliance into business value

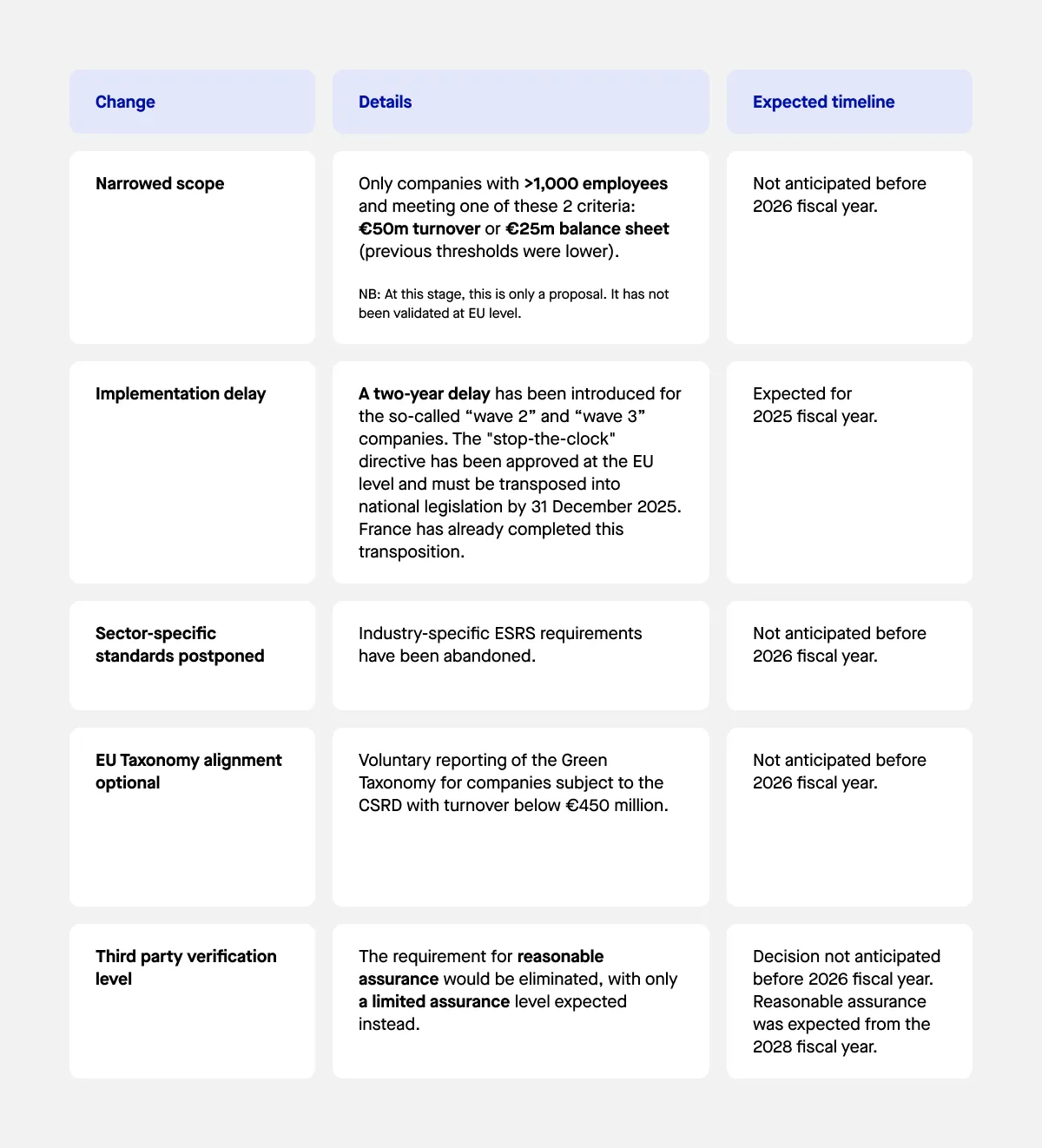

Over the past few months, the Omnibus proposals have led the European Commission to reassess the scope and content of the CSRD. While discussions are still ongoing, the two‑year implementation delay, which has already been approved, means “Wave 2” companies will publish their CSRD reports in early 2028, covering the 2027 fiscal year. If you’re among these companies, you should start preparing now.

Under the CSRD’s current rollout schedule, the so-called “wave 2 companies” were originally expected to publish their first sustainability report in early 2026, covering the 2025 financial year. However, the latest omnibus proposal introduces a two-year delay, meaning these companies would now only need to report in 2028, based on 2027 financial data.

At the same time, the thresholds for inclusion are being revised. Under the proposal, wave 2 companies will be those with more than 1,000 employees and a net turnover above €450 million, provided they are not already covered as wave 1 companies.

Looking ahead, other businesses will also fall within the scope of the CSRD, including non-EU companies. For these, the first reports would be due in 2029, based on 2028 financial year data.

On 26 February 2025, the European Commission introduced two legislative proposals to amend the Corporate Sustainability Reporting Directive (CSRD): the so-called “stop-the-clock” directive and the “content” directive. These proposals aim to simplify and clarify aspects of the CSRD while maintaining its core objectives of transparency and accountability in sustainability reporting across the European Union.

Together, the proposals adjust compliance timelines, reduce administrative burdens, and refine key obligations – particularly for companies newly subject to CSRD requirements. They also clarify the relationship between EU-level rules and national laws across member states, supporting more consistent implementation of sustainability reporting standards.

Importantly, the proposals reaffirm the emphasis on general disclosures related to climate change and companies’ progress toward net zero emissions. They align with the European Parliament’s broader environmental agenda and reinforce the importance of robust sustainability reporting. Organizations preparing for CSRD compliance should monitor both proposals closely and update their reporting strategies as needed.

The CSRD was designed to expand and improve upon the Non-Financial Reporting Directive (NFRD), with the aim of enhancing corporate accountability and transparency. It requires companies to disclose environmental, social, and governance (ESG) information alongside their financial results.

To standardize how these disclosures are made, the European Sustainability Reporting Standards (ESRS) were created by EFRAG (European Financial Reporting Advisory Group). These standards form the foundation of CSRD compliance and ensure consistency across all sectors and member states.

The double materiality principle remains at the core of the CSRD. This means companies must evaluate and disclose:

This approach helps companies identify which sustainability matters are material, and should be included in the sustainability report. It ensures that sustainability reporting is both relevant for investors and stakeholders and reflective of real-world impacts.

As of the end of July 2025, the proposed revisions to the ESRS include a 57% reduction in mandatory data points, a 68% cut in total disclosures, and the removal of all voluntary (“may”) disclosures. Despite this streamlining, companies reporting in 2027 will still be expected to provide clear, detailed, and verifiable sustainability data on their material topics, across three key ESG areas:

Note that the bullet points below are not exhaustive, and are subject to the given organization’s double materiality analysis.

In line with the Global Reporting Initiative (GRI) and the ISSB’s IFRS S1/S2 standards, CSRD reporting is designed to harmonize with global frameworks, offering businesses a cohesive and integrated way to report across jurisdictions.

For companies beginning their sustainability journey, 2027 may feel like a distant milestone. However, the scale and complexity of the CSRD disclosure requirements mean that early preparation is essential – especially for businesses that have never produced formal ESG reporting or those unfamiliar with the European Sustainability Reporting Standards (ESRS).

Building a robust foundation now can help organizations avoid last-minute scrambles, ensure accurate reporting, and make the most of sustainability as a performance driver. Below are seven practical steps to begin the journey to compliance.

Double materiality is at the heart of the CSRD and ESRS. Companies must assess both financial materiality (how sustainability risks affect the business) and impact materiality (how the business affects people and the environment).

Conducting this assessment early helps determine which disclosure requirements apply to your company – filtering out irrelevant data points and focusing your reporting efforts where they matter most. It also informs the subsequent gap analysis, ensuring you’re only evaluating what’s necessary.

Tip: Start with value chain and risk mapping to identify where your company’s operations directly or indirectly intersect with key sustainability topics.

Once you’ve established what’s material, assess your current policies, data systems, and sustainability disclosures against the relevant ESRS. A detailed gap analysis helps identify where improvements are needed – particularly in areas like value chain data, social and environmental metrics, and governance structures.

Early identification of these gaps allows for smarter prioritization, budgeting, and alignment with internal teams and external partners.

Sustainability reporting is only as strong as the data behind it. Companies must establish strong data governance practices to ensure the consistency, reliability, and auditability of their sustainability metrics. This includes centralizing carbon emissions data, workforce diversity indicators, energy consumption, and governance practices.

Since CSRD disclosure forms part of the annual report, the integrity of ESG data must match that of financial data. Companies must demonstrate that their information is complete, reliable, and aligned with ESRS expectations.

Complying with CSRD cannot be done in isolation. A successful approach involves cross-functional collaboration across departments such as finance, HR, legal, procurement, and operations, as well as engagement with other stakeholders . Externally, engagement with suppliers, auditors, and other value chain partners is critical.

Engaging these stakeholders early supports a more comprehensive understanding of risks posed by sustainability factors across the value chain. It also encourages ownership and accountability within teams, which is essential for collecting the sustainability information required and embedding ESG into day-to-day business operations.

The technical and administrative burden of CSRD compliance can be significant. ESG software platforms are purpose-built to ease this load. The right tools can:

By embedding technology into your reporting processes early, you can improve accuracy, reduce manual effort, and scale as new disclosure requirements emerge.

One of the more significant additions under the CSRD is the requirement for external assurance of sustainability information.

Building a relationship with an assurance provider now will help you define clear validation processes and avoid delays as deadlines approach. This is especially important for areas where ESG data may be unstructured or spread across multiple business units or geographies.

The CSRD doesn’t exist in a vacuum. Many of its core principles, particularly around double materiality, reflect broader global shifts in ESG reporting. In fact, we anticipate significant overlap between the indicators required by CSRD, ISSB IFRS S1/S2, and GRI.

For companies operating internationally, this presents a strategic opportunity: using ESG software, they can create interoperable indicators from the outset, and in doing so, ensure that what’s reported under one framework can be efficiently adapted for another. This alignment not only reduces duplication of effort but sets the foundation for a more streamlined, scalable, and consistent global reporting strategy

Consider aligning your reporting with:

Using CSRD as a strategic anchor, companies can enhance their overall ESG reporting maturity and reduce the duplication of efforts across jurisdictions.

In-scope businesses need to disclose the sustainability information in their management reports, which means that financial and sustainability information should be published at the same time.

CSRD compliance isn’t limited to EU-based businesses. Non-EU companies may also fall within scope, starting with the 2028 fiscal year. This means that their first reports would be published in 2029. This timeline is not under debate in the current Omnibus proposal; what is being discussed is which non-EU companies will be included.

According to the Omnibus proposal, the criteria for non-EU companies to fall under CSRD include:

Although these thresholds are still under discussion and not yet finalized, they signal a strong direction of travel. In parallel, the Commission has indicated plans to publish a separate set of ESRS tailored for non-EU companies, though no updates have been released since the omnibus proposal was announced.

For multinational organizations, this brings added complexity – particularly around cross-border data collection, jurisdictional alignment, and adapting global ESG frameworks to meet the granular requirements of ESRS.

Tip: If you’re a European branch or subsidiary of a non-EU parent company that will fall into CSRD scope later, your own reporting preparation is critical. Your disclosures can lay the groundwork and become a valuable reference point for the group’s future compliance efforts.

While legal compliance is a core driver, forward-thinking businesses view sustainability reporting as a value-creation tool. High-quality CSRD disclosure enables companies to:

Companies that integrate sustainability into core strategy will be better equipped to respond to evolving stakeholder expectations and shifting market dynamics.

Although the Omnibus Proposal may delay compliance for some and reduce the scope for others, the core of the CSRD remains intact. The requirements for double materiality assessment, external assurance, digital tagging, and the inclusion of sustainability information in the annual report are not going away.

Organizations set to report in 2027 must start building their internal architecture now. This includes:

By taking these steps, companies can transform compliance from a regulatory burden into a strategic advantage – strengthening transparency, building trust, and advancing the transition to a more sustainable and responsible economy.

Focus on what’s material

Run your double materiality assessment with CSRD-ready workflows. Set thresholds so your report highlights only the ESG topics that matter most.

Spot and close data gaps

Map every required datapoint, flag missing information, and automate data collection across teams and value chain partners.

Enable cross-functional collaboration

Make it easy for finance, HR, legal, procurement, and operations to input, validate, and track ESRS data in one place.

Track readiness in real time

Use dashboards to see progress, identify strong coverage, and spot gaps across material topics and ESRS sections.

Simplify audits and assurance

Rely on validation checks, approval flows, and audit trails. Lock disclosures with data snapshots to prepare for external review.

Turn compliance into value

Use CSRD and ESRS data to set targets, model scenarios, and drive transition plans that deliver ROI and accelerate progress toward net zero.

Sweep makes sustainability work for your business. Not the other way round. We connect all your sustainability data and turn it into business intelligence to help you unlock performance – from compliance and risk reduction, all the way to cost-savings, and market differentiation.

With Sweep, you can: