The California Air Resources Board (CARB) has published a new draft reporting template for SB 253, the Climate Corporate Data Accountability Act. This landmark law is part of California’s climate disclosure laws and requires companies doing business in California with total annual revenues exceeding $1 billion to report their greenhouse gas (GHG) emissions each year.

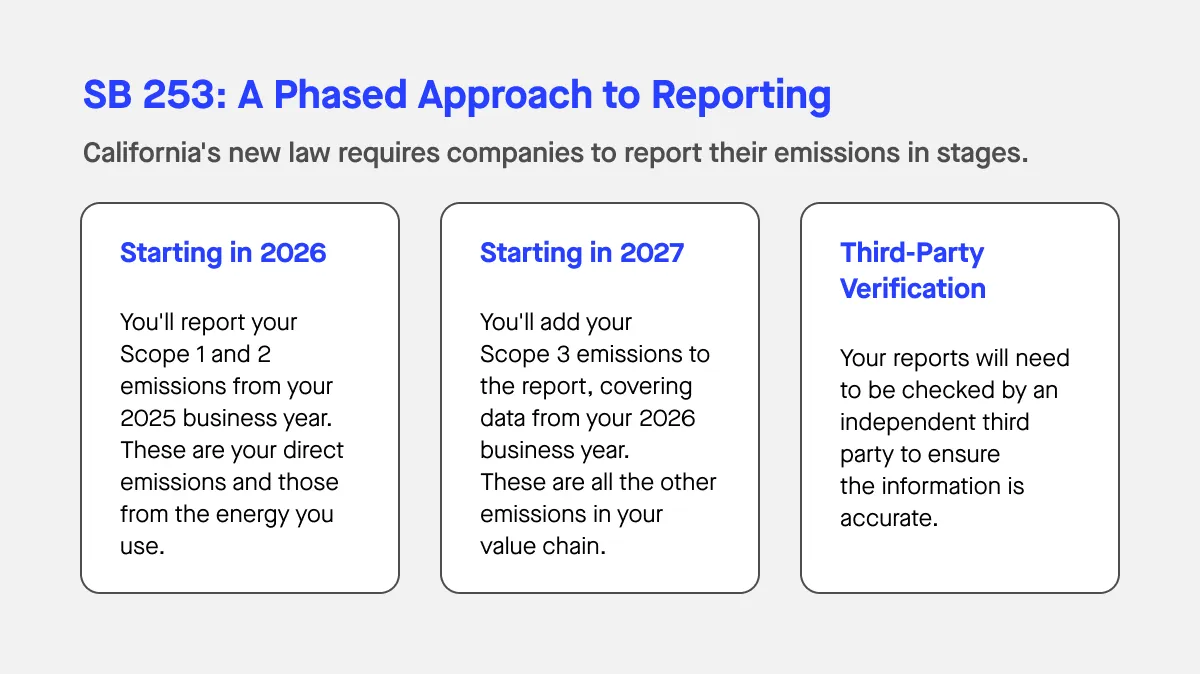

CARB’s proposed reporting framework – released in Excel format – sets out the data fields that reporting entities will use to disclose Scope 1 (direct) and Scope 2 (indirect) greenhouse gas emissions beginning in 2026, covering fiscal 2025. While use of the template is voluntary for the first cycle, it marks an important step toward standardized, publicly accessible climate disclosures in the U.S.

Below, we answer the key questions about this new California law, how companies can begin preparing, and how ESG software can help manage complex emissions reporting efficiently and accurately.

What is the new template designed to do?

CARB stated that the template is intended to streamline the reporting process for large businesses and private companies subject to California’s Climate Corporate Data Accountability Act. It provides a consistent structure to capture essential emissions data and helps entities – particularly those disclosing for the first time – understand what must be publicly reported under SB 253.

The template is also designed to support good faith efforts at compliance during the first reporting timelines in 2026. Companies are encouraged to use the format to ensure data comparability across sectors and to align with the Greenhouse Gas Protocol (GHG Protocol).

CARB reiterated that the file is a guidance document, not a legally binding instrument. It does not replace or modify the bill text of California SB 253 or other climate disclosure laws, but it offers a reasonable basis for reporting entities to start organizing data, setting boundaries, and engaging third-party assurance providers.

Which greenhouse gas emissions scopes are covered in the template?

The draft CARB proposed template covers Scope 1 and Scope 2 GHG emissions, which companies must disclose starting in 2026.

- Scope 1 emissions include direct releases from owned or controlled sources – such as stationary and mobile combustion, process emissions, and fugitive emissions.

- Scope 2 emissions cover indirect emissions from purchased electricity, heating, steam, or cooling used in operations.

Each reporting entity must also indicate whether its organizational boundary is based on an equity share, financial control, or operational control approach, in line with the GHG Protocol.

While Scope 3 emissions (value chain and supply chain impacts) are not yet included in this draft, SB 253 requires disclosure of these indirect emissions beginning in 2027 for fiscal 2026. Companies will need to track emissions across their supply chains to comply with these future reporting requirements. CARB confirmed it will release a separate template and additional workshops to support that next phase of reporting requirements.

At the end of the process, CARB’s list will identify which companies are required to comply with SB 253 based on the established criteria.