California’s SB 253 is one of the strictest climate disclosure laws in the US and aligns with global sustainability reporting frameworks. All emissions disclosures must be verified by an independent third party. Organizations that fail to comply may face administrative penalties of up to $500,000 per year.

Related legislation, SB 261, addresses climate related financial risks and requires separate climate-related financial risk disclosures.

Who oversees compliance and enforcement

The role of CARB

The California Air Resources Board (CARB), is responsible for overseeing compliance with SB 253 and developing implementation rules for emissions reporting. CARB will ensure verification of data by a registry or third-party auditor with expertise in carbon accounting and global greenhouse gas accounting.

Penalties and enforcement approach

The California Air Resources Board can impose administrative penalties for non-compliance. CARB has noted that reporting entities making a good faith effort in the initial cycle will receive enforcement flexibility.

An emissions reporting organization shall not be subject to an administrative penalty for any misstatements regarding Scope 3 emissions disclosures made with a reasonable basis and disclosed in good faith. Penalties assessed on Scope 3 reporting between 2027 and 2030 shall only occur for nonfiling – supporting timely reporting implementation.

What must be assured

Phased assurance requirements

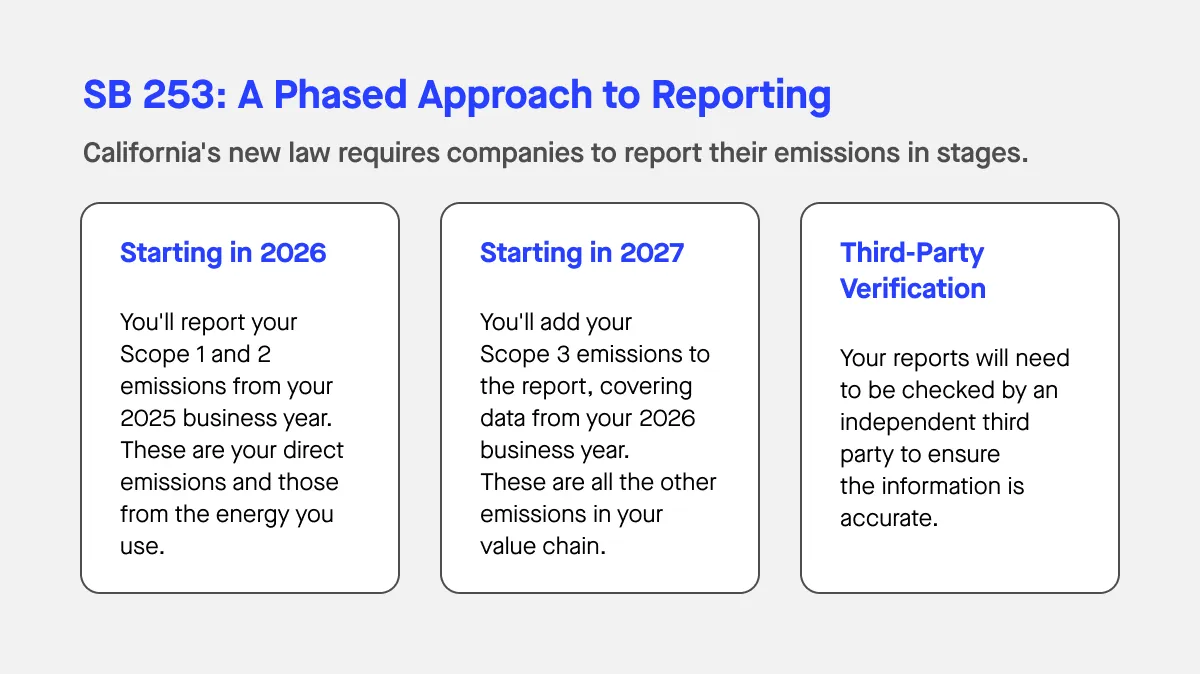

CARB has signaled that companies should prepare for a phased assurance approach. The assurance engagement for Scope 1 and Scope 2 emissions will be performed at a limited assurance level beginning in 2026 and at a reasonable assurance level beginning in 2030.

For Scope 3 emissions, which often account for more than 90% of an organization’s climate impact and are notoriously difficult to measure, the state board will review and evaluate trends in third-party assurance requirements during 2026. The assurance engagement for Scope 3 emissions will be performed at a limited assurance level beginning in 2030.

Standards and protocols

Reports under SB 253 must follow the Greenhouse Gas Protocol, which is the widely recognized standard for measuring and managing emissions.

The assurance process minimizes the need for reporting entities to engage multiple assurance providers, though some may choose to work with multiple assurance providers based on geographic or operational complexity. The complete assurance provider’s report must meet specifications defined by regulations adopted pursuant to SB 253.

What auditors look for

Independent third-party assurance is required to verify the accuracy and completeness of emissions disclosures under California SB 253. A third-party assurance provider must have significant experience in measuring, analyzing, reporting, or attesting to greenhouse gas emissions and corporate GHG emissions accounting.

Assurance providers apply well-established audit principles. Even as CARB finalizes the rules, most auditors will focus on several consistent themes.

Clear and justified boundaries

Organizational boundary approaches

CARB’s draft template for Scope 1 and Scope 2 requires an emissions reporting organization pursuant to SB 253 to disclose which organizational boundary approach they use: operational control, financial control, or equity share. Auditors will want to see a written rationale for this choice and a clear explanation of which locations, assets, and subsidiaries are included in the greenhouse gas emissions inventory.

Understanding the three scopes

Scope 1 emissions are all direct greenhouse gas emissions that stem from sources a reporting entity owns or directly controls.

Scope 2 emissions are indirect greenhouse gas emissions from consumed electricity, steam, heating, or cooling purchased or acquired by a reporting entity.

Scope 3 emissions are indirect upstream and downstream greenhouse gas emissions from sources the reporting entity does not own or directly control.

Each scope requires clear boundary documentation that supports comprehensive GHG emissions data collection.

Traceable data and evidence files

What auditors verify

Every figure in the greenhouse gas emissions inventory must be linked to a verifiable source. Auditors will check that invoices, metering data, travel records, supplier submissions, and system extracts match the values shown in calculations. This is fundamental to accurate and comprehensive data reporting.

Building your evidence file

An evidence file is a structured collection of source documents that supports each data point in your emissions data. Key components include:

- Utility bills and meter readings for electricity, natural gas, and other energy sources

- Fuel purchase receipts for company vehicles and equipment

- Travel and expense reports showing business mileage and air travel

- Supplier-specific emissions data or industry average data when direct data is unavailable

- System exports from ERP or procurement platforms

- Calculation sheets showing how raw data was converted to emissions totals

- Emission factor sources with publication dates

Auditors will sample data points across your inventory and trace them back to supporting documentation. For Scope 3, auditors will examine how you distinguish between supplier-specific data, industry average data, and estimates. CARB will require companies to describe methodology and any minor or de minimis sources.

Evidence management best practices

- Centralize files in a single platform organized by scope and reporting period

- Use consistent naming conventions

- Version control calculations

- Document assumptions in writing

- Retain files for at least five years

Accurate methods and emission factors

Following recognized standards

Assurance teams look for calculations that follow the Greenhouse Gas Protocol and support global GHG emissions reporting. CARB’s workshop materials show that companies will need to specify emission factor sources and dates, ensuring compliance with globally recognized alternative accounting standards where applicable.

Year-over-year consistency

Auditors verify that emission factors are current, from credible sources, and applied correctly. If a method changes from one year to the next, auditors expect a clear explanation, especially as companies refine their corporate carbon emissions accounting practices.

Strong controls and defined responsibilities

Internal control requirements

SB 253 pushes companies toward a more controlled reporting environment. The assurance process ensures sufficient assurance provider capacity while raising the bar for internal rigor in corporate carbon emissions reporting.

Auditors will look for:

- Defined responsibilities for data owners and reviewers

- Documented procedures for data collection and validation

- Change control for calculations and templates

- Review and approval steps that mirror financial reporting discipline

Ownership and accountability

This means someone must own each emissions category, review supplier data before it enters the inventory, and sign off on the reporting entity’s public disclosure before it becomes publicly accessible.

Building the right data infrastructure

Why sustainability data management matters

Companies will need to develop internal systems for tracking global emissions to comply with SB 253. Sustainability data management systems are essential for tracking and reporting greenhouse gas emissions accurately and supporting greenhouse gas emissions disclosure requirements.

Organizations must implement robust data management platforms to centralize emissions reporting and ensure accuracy. These platforms facilitate the collection of emissions data from various sources, including suppliers and utility bills, and should be integrated with existing business processes to ensure compliance with regulatory frameworks.

Leveraging technology

The use of AI-powered tools in sustainability data management can improve data accuracy and reduce reliance on manual estimates. These tools can flag anomalies, suggest emission factors, and map supplier data to correct categories in the greenhouse gas emissions reporting program.

Consistency, transparency, and climate accountability

The shift to mandatory disclosure

California’s SB 253 represents a significant shift in climate accountability and climate corporate data accountability by mandating large organizations to publicly disclose their GHG emissions. The law aims to reduce ‘greenwashing’ and increase corporate transparency regarding climate change impact, while protecting investors from climate related financial risks.

Documentation requirements

Auditors expect consistency year over year in emissions reporting. If you change your boundary, switch emission factor sources, or refine your Scope 3 methodology, document why and quantify the impact. CARB’s regulations adopted pursuant to the health and safety code will require reconciliation of any material changes.

Transparency extends to uncertainty. If you rely on industry average data or estimates for downstream greenhouse gas emissions, disclose this clearly in your corporate climate disclosure.

Preparing for assurance under SB 253

Start early

Organizations must secure third-party assurance early to avoid bottlenecks as reporting deadlines approach due to limited qualified auditors. Start your readiness work now:

Six essential steps

- Map your emissions sources across all scopes and build your organizational boundary

- Centralize data collection using sustainability data management systems

- Build evidence files for every emissions category

- Document your methodology in a written emissions accounting manual

- Conduct an internal review before engaging your assurance provider

- Engage your auditor early to discuss scope and timing

Next steps

The shift from voluntary reporting to mandatory industrial emissions disclosure is underway. The implementation of SB 253 is part of a broader legislative push to ensure corporate accountability in climate action and statewide greenhouse gas emissions reduction.

If you need support building a compliance-ready greenhouse gas emissions inventory, documenting controls, or preparing for third-party assurance, Sweep’s platform centralizes emissions data, automates evidence management, and applies the Greenhouse Gas Protocol corporate standards across your global operations.

The assurance process doesn’t have to be overwhelming. With the right systems and documentation practices, you can meet California’s requirements while building a foundation for credible climate disclosure.