What’s changed after the Omnibus announcement?

In July 2025, the European Commission proposed amendments to simplify CSRD reporting without weakening its goals. These changes followed significant input from businesses and aim to reduce complexity while maintaining the directive’s focus on transparency and accountability.

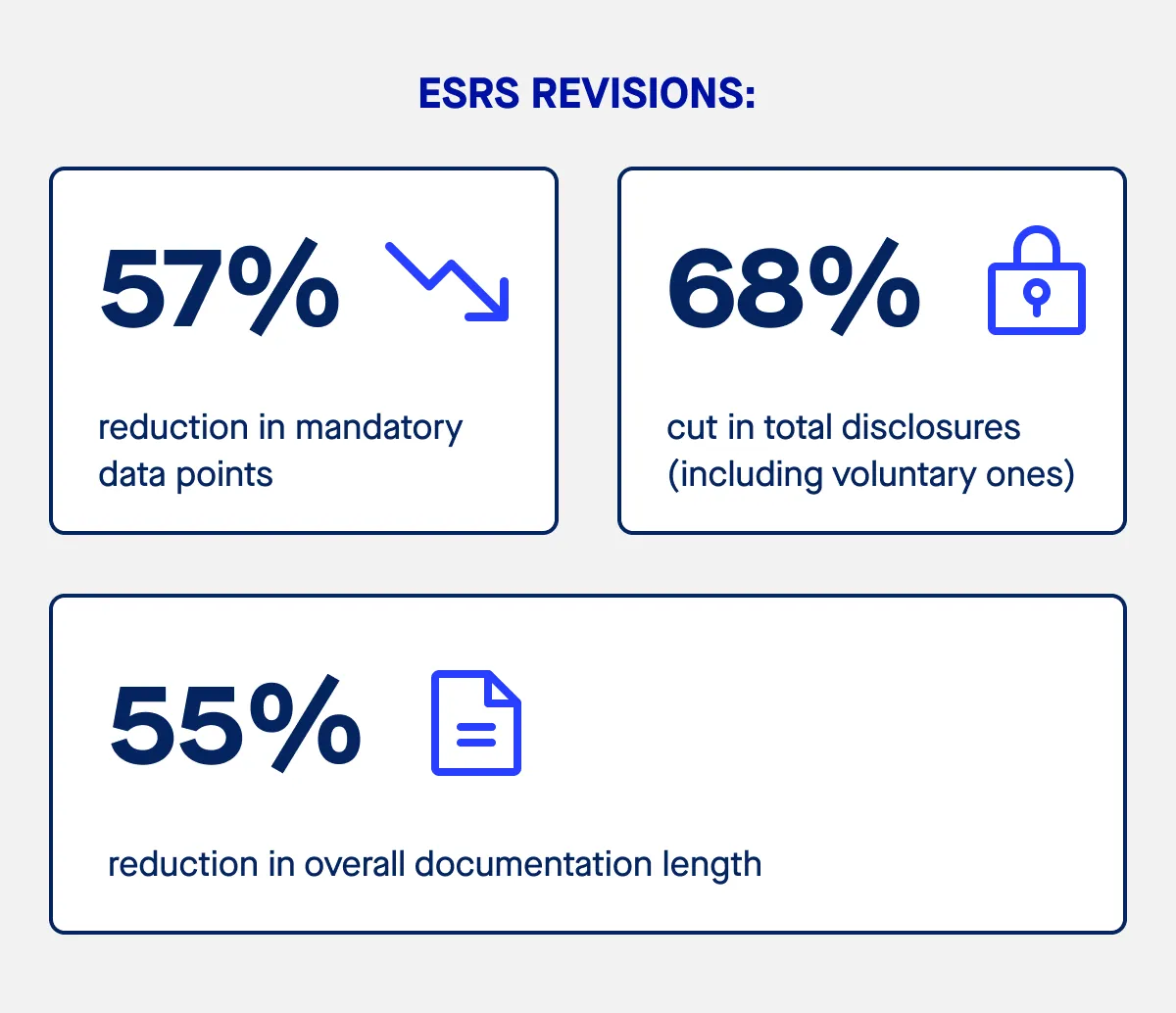

Key updates include:

- A 57% reduction in mandatory data points

- Removal of all voluntary “may” disclosures

- A 68% cut in total disclosures

- The option to move detailed data into appendices rather than the main body of reports

- Postponement of the reasonable assurance requirement, with limited assurance continuing for now

Scope and timing changes

- Wave 2 and 3 companies will now report from fiscal years starting 2028–2029

- Voluntary reporting standards are available for very small and medium sized enterprises

- Adjusted thresholds for CSRD disclosure for some EU subsidiaries of global groups

These reforms are designed to make it easier for more companies to meet regulatory requirements while maintaining a consistent standard of sustainability reporting across member states.

Why UK businesses should act now

The business case for readiness

If your organisation meets the CSRD requirements, your first step is a double materiality assessment, considering both financial materiality and the impact of your business activities on social and environmental issues. This assessment helps identify which sustainability matters are most relevant to your operations, your financial results, and your stakeholders.

Failing to prepare could impact access to EU regulated markets, investor confidence, and your position in global value chains that prioritise social responsibility and the circular economy. It may also limit your ability to meet transition plans and sustainability goals. With the European Parliament moving ahead, companies that comply sooner will be better placed to demonstrate leadership in corporate sustainability and gain a competitive advantage.

How ESG software can help with CSRD compliance

Simplifying complex reporting obligations

Meeting CSRD requirements can be resource-intensive, especially for UK companies that are new to EU reporting frameworks. ESG tools and platforms can help companies:

- Centralise sustainability information and non-financial data

- Align reports with the sustainability reporting directive CSRD, ESRS, and the EU taxonomy

- Enable accurate, timely, and compliance-ready outputs

- Integrate sustainability and financial reporting systems

Benefits for UK companies

- Reduce manual work and reporting errors

- Improve visibility of sustainability risks across the value chain

- Enhance tracking of sustainability performance

- Meet regulatory requirements efficiently

- Provide essential information to investors, consumers, and stakeholders

Staying ahead of EU sustainability reporting standards

CSRD introduces new topical standards covering climate change, human rights, environmental impacts, and sustainability matters across your operations and supply chain.

For UK businesses, the best approach is to:

- Map your scope and obligations early

- Put in place strong reporting and governance processes

- Involve leadership and supply chain partners in sustainability initiatives

- Use technology to ensure compliance and improve decision making

By acting now, UK companies can not only comply with the CSRD but also strengthen their corporate sustainability reporting, improve transparency, and create long-term value in the European Union market.